Skewed Normal Distribution | ||||

|

| |||

The skewed normal distribution is defined by three parameters (Owen, 1956):

-

skewness ,

-

strictly positive scale , and

-

location .

A normal distribution is obtained when the skewness is zero (i.e., ![]() ). The direction in which the distribution is skewed

depends on the sign of

). The direction in which the distribution is skewed

depends on the sign of  .

.

The skewed normal cumulative distribution function is

where is the Owen’s T-function,

The mean and standard deviations for the skewed normal distribution are

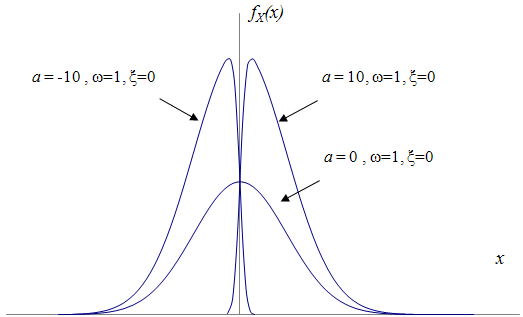

The skewed normal probability density function, as shown in the following figure,

is

where is the standard normal probability density function and is the standard normal cumulative distribution function.